az

az ru

ru tr

tr

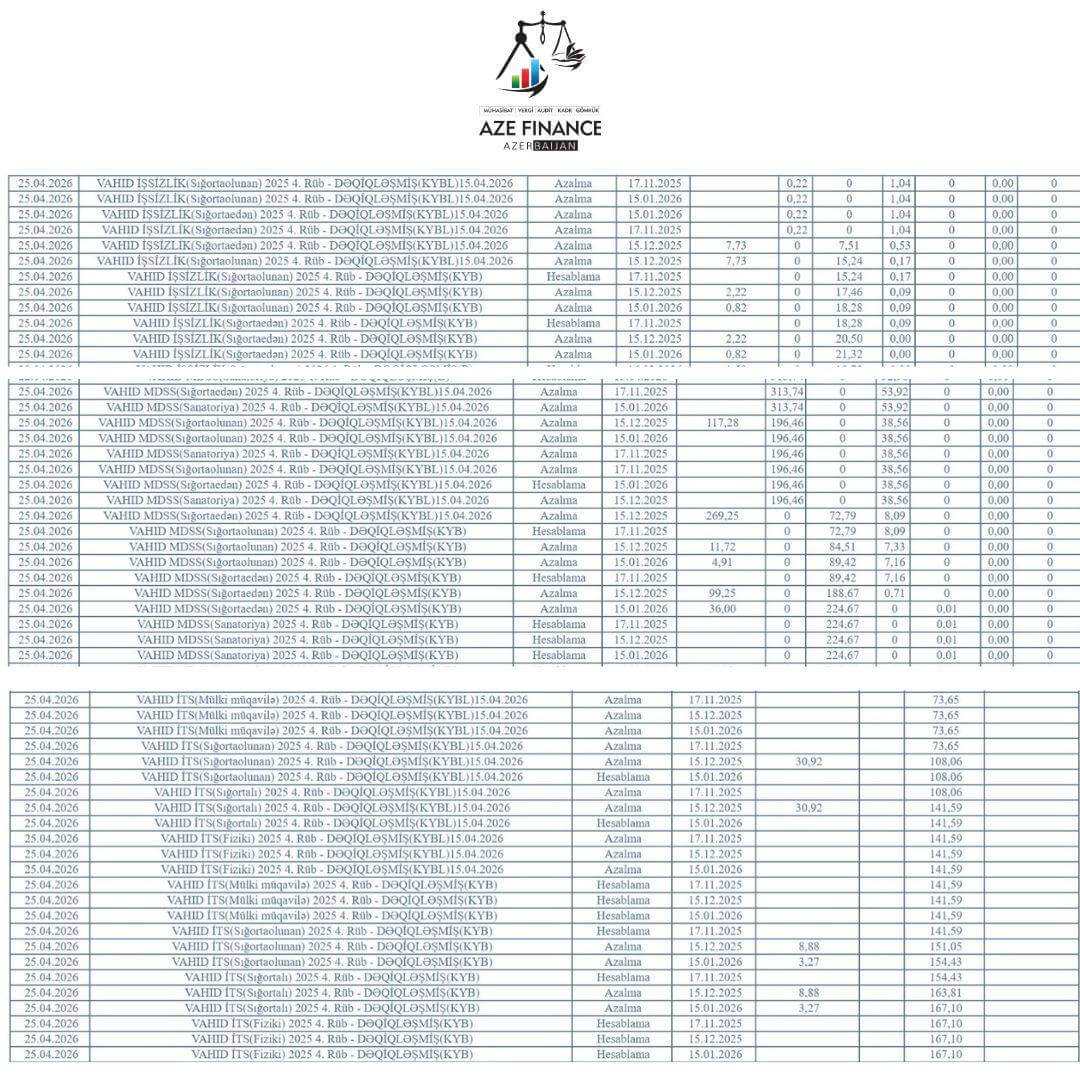

Decrease in the unified tax return for the fourth quarter of 2025

As a result of adjustments made to the unified tax return for the fourth quarter of 2025, a total decrease of 646.09 AZN was recorded in social and mandatory payments related to salaried employment. This decrease was formed as follows:

- Unemployment insurance contribution: 21.54 AZN decrease

- Mandatory state social insurance (MDSS): 538.41 AZN decrease

- Compulsory health insurance: 86.14 AZN decrease

Following these corrections, the overall reduction in the unified tax return was balanced, and the reporting indicators were updated in accordance with legal requirements. These changes were implemented to eliminate inconsistencies in the initially submitted data, ensure accurate calculations, and align payments with actual figures.

The adjustment process was carried out with the involvement of relevant specialists, calculations were thoroughly reviewed, and each indicator was clarified. The support of Ishak Gasimov and the execution by Ulviyya Nagiyeva played a significant role in this process.

As a result, the updated data for the unified tax return for the fourth quarter of 2025 is considered more accurate and reliable from a financial and tax accounting perspective. Such adjustments are crucial for ensuring proper future reporting, preventing potential financial risks, and maintaining a transparent accounting system.

As a result of adjustments made to the unified tax return for the fourth quarter of 2025, a total decrease of 646.09 AZN was recorded in social and mandatory payments related to salaried employment. This decrease was formed as follows:

- Unemployment insurance contribution: 21.54 AZN decrease

- Mandatory state social insurance (MDSS): 538.41 AZN decrease

- Compulsory health insurance: 86.14 AZN decrease

Following these corrections, the overall reduction in the unified tax return was balanced, and the reporting indicators were updated in accordance with legal requirements. These changes were implemented to eliminate inconsistencies in the initially submitted data, ensure accurate calculations, and align payments with actual figures.

The adjustment process was carried out with the involvement of relevant specialists, calculations were thoroughly reviewed, and each indicator was clarified. The support of Ishak Gasimov and the execution by Ulviyya Nagiyeva played a significant role in this process.

As a result, the updated data for the unified tax return for the fourth quarter of 2025 is considered more accurate and reliable from a financial and tax accounting perspective. Such adjustments are crucial for ensuring proper future reporting, preventing potential financial risks, and maintaining a transparent accounting system.