In what cases can the tax payment deadline be extended?

In what cases can the tax payment deadline be extended?

The deadlines for fulfilling tax obligations and the rules for changing these deadlines are explained by expert Elshad Ahmadli:

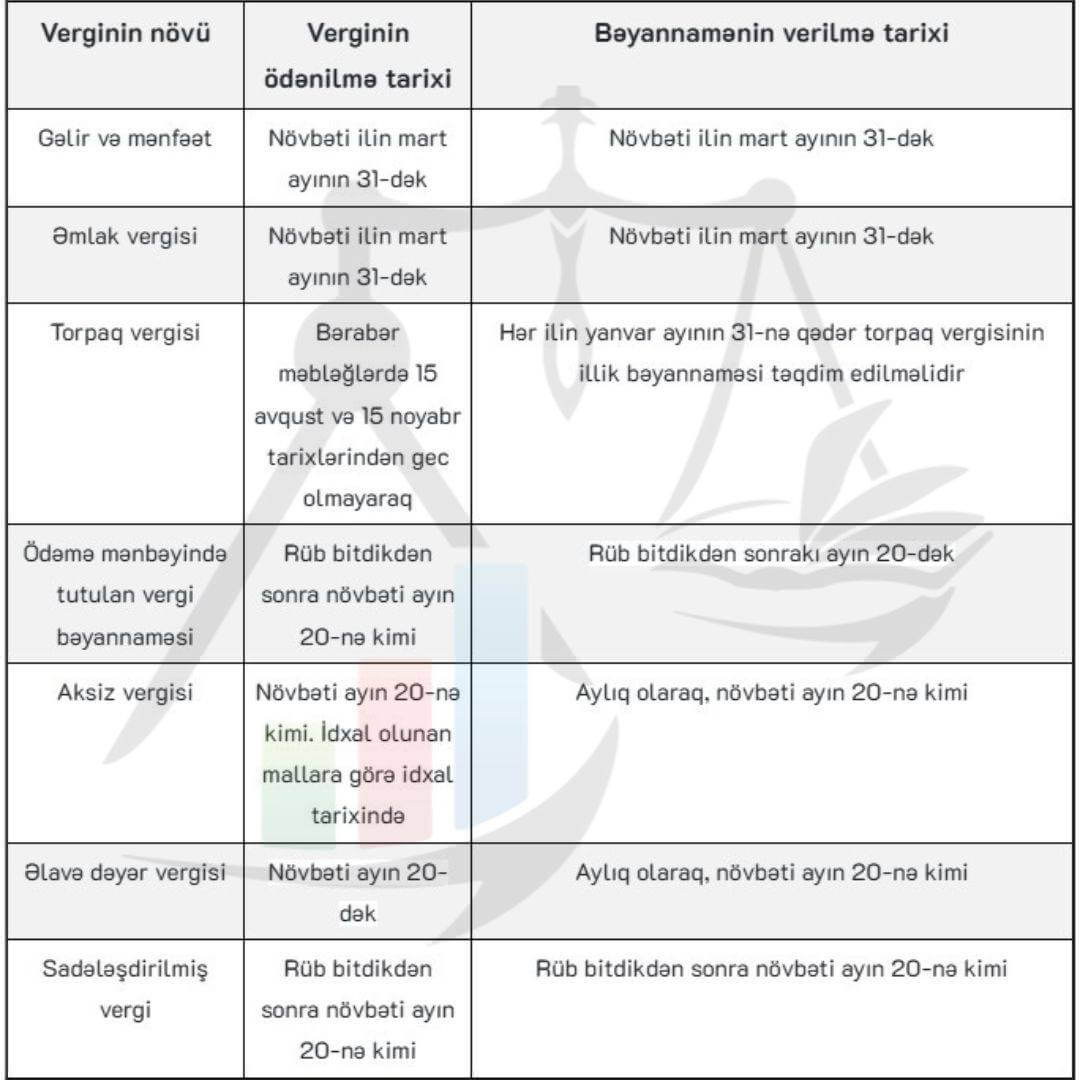

In accordance with Article 85.1 of the Tax Code, the deadlines for payment of each tax have been established. Changing the payment deadlines can only be carried out in accordance with the procedure established by this Code. According to tax legislation, the following deadlines have been established for the payment of the main taxes:

According to Article 59.1 of the Tax Code, if a tax or current tax payment is not paid within the period established by this Code, interest in the amount of 0.1 percent of the unpaid tax or current tax payment shall be charged from the taxpayer or tax agent for each past due day after the payment deadline.

Example 1: Since the taxpayer submitted the simplified tax return for the 2nd quarter of 2024 on July 5, 2024, a debt of 381 manat arose as of that date. However, interest is not charged to the taxpayer for the past day, since the last date for payment of the simplified tax for the 2nd quarter is considered to be July 22, 2024. It should be noted that the simplified tax amount must be paid by the 20th of the month following the end of the quarter. In this example, the time has been extended since it falls on a non-working day.

Example 2: Current tax payments must be paid by the 15th of the month following each reporting quarter. If the taxpayer has not made the payment within that time, interest is charged in the amount of 0.1% of the current tax amount in accordance with Article 59.1 of the Tax Code.

Example 3: The VAT report for January was submitted on February 15. The VAT debt amount incurred was 500 manats. The obligation was paid on March 10. In this case, 0.1 percent is calculated for each day after February 20:

(500 x 18 days) x 0.1% = 9 manats.

According to Article 85.6.1 of the Tax Code, taxpayers are allowed to extend the period for fulfilling their tax obligations if they suffer losses as a result of natural disasters, accidents at hazardous facilities, and other unavoidable processes. To do this, taxpayers must obtain certificates from the relevant state bodies regarding the damage and apply to the tax authority with these certificates. This will help them gain additional time in fulfilling their tax obligations.

Each application must be made in accordance with the relevant rules so that the tax authorities can take these requirements into account. In this process, payment of 10 percent of the tax debt is also required. Thus, taxpayers can fulfill their tax obligations on time, reducing the impact of natural disasters. If a taxpayer suffers damage as a result of a natural disaster or force majeure, interest is not calculated on the extension of the tax payment period. This aims to reduce the financial burden of the taxpayer and facilitate their recovery process.

To extend the period for fulfilling tax obligations, the taxpayer must submit the following documents:

- a reasoned application for the extension of the period;

- a certificate from the relevant body regarding the occurrence of the event;

- a certificate from the relevant body regarding the amount of damage caused as a result of the event.

If these grounds are presented, the taxpayer may extend the payment period from 1 to 9 months during the tax year. This helps enterprises to continue their activities by creating more comfortable conditions for recovering losses.

The period for fulfilling an extended tax obligation may be terminated early in the following cases:

- when the taxpayer fulfills the tax obligation ahead of schedule;

- when a criminal case is initiated against the taxpayer for violating tax legislation;

- when the terms of the decision on extending the period for fulfilling the tax obligation are not complied with.

Also, the tax authority must inform the taxpayer about the early termination of the extended period within 5 days. The taxpayer must pay the debt amount and accrued interest on that amount within 30 days from the date of receipt of this information. These procedures increase the responsibility of taxpayers and ensure their compliance with the legislation.

The taxpayer has the right to complain about the actions or inaction of the tax authority, as well as their officials, regarding the premature termination of the extended period for fulfilling the tax obligation.

The deadlines for fulfilling tax obligations and the rules for changing these deadlines are explained by expert Elshad Ahmadli:

In accordance with Article 85.1 of the Tax Code, the deadlines for payment of each tax have been established. Changing the payment deadlines can only be carried out in accordance with the procedure established by this Code. According to tax legislation, the following deadlines have been established for the payment of the main taxes:

According to Article 59.1 of the Tax Code, if a tax or current tax payment is not paid within the period established by this Code, interest in the amount of 0.1 percent of the unpaid tax or current tax payment shall be charged from the taxpayer or tax agent for each past due day after the payment deadline.

Example 1: Since the taxpayer submitted the simplified tax return for the 2nd quarter of 2024 on July 5, 2024, a debt of 381 manat arose as of that date. However, interest is not charged to the taxpayer for the past day, since the last date for payment of the simplified tax for the 2nd quarter is considered to be July 22, 2024. It should be noted that the simplified tax amount must be paid by the 20th of the month following the end of the quarter. In this example, the time has been extended since it falls on a non-working day.

Example 2: Current tax payments must be paid by the 15th of the month following each reporting quarter. If the taxpayer has not made the payment within that time, interest is charged in the amount of 0.1% of the current tax amount in accordance with Article 59.1 of the Tax Code.

Example 3: The VAT report for January was submitted on February 15. The VAT debt amount incurred was 500 manats. The obligation was paid on March 10. In this case, 0.1 percent is calculated for each day after February 20:

(500 x 18 days) x 0.1% = 9 manats.

According to Article 85.6.1 of the Tax Code, taxpayers are allowed to extend the period for fulfilling their tax obligations if they suffer losses as a result of natural disasters, accidents at hazardous facilities, and other unavoidable processes. To do this, taxpayers must obtain certificates from the relevant state bodies regarding the damage and apply to the tax authority with these certificates. This will help them gain additional time in fulfilling their tax obligations.

Each application must be made in accordance with the relevant rules so that the tax authorities can take these requirements into account. In this process, payment of 10 percent of the tax debt is also required. Thus, taxpayers can fulfill their tax obligations on time, reducing the impact of natural disasters. If a taxpayer suffers damage as a result of a natural disaster or force majeure, interest is not calculated on the extension of the tax payment period. This aims to reduce the financial burden of the taxpayer and facilitate their recovery process.

To extend the period for fulfilling tax obligations, the taxpayer must submit the following documents:

- a reasoned application for the extension of the period;

- a certificate from the relevant body regarding the occurrence of the event;

- a certificate from the relevant body regarding the amount of damage caused as a result of the event.

If these grounds are presented, the taxpayer may extend the payment period from 1 to 9 months during the tax year. This helps enterprises to continue their activities by creating more comfortable conditions for recovering losses.

The period for fulfilling an extended tax obligation may be terminated early in the following cases:

- when the taxpayer fulfills the tax obligation ahead of schedule;

- when a criminal case is initiated against the taxpayer for violating tax legislation;

- when the terms of the decision on extending the period for fulfilling the tax obligation are not complied with.

Also, the tax authority must inform the taxpayer about the early termination of the extended period within 5 days. The taxpayer must pay the debt amount and accrued interest on that amount within 30 days from the date of receipt of this information. These procedures increase the responsibility of taxpayers and ensure their compliance with the legislation.

The taxpayer has the right to complain about the actions or inaction of the tax authority, as well as their officials, regarding the premature termination of the extended period for fulfilling the tax obligation.